Cover Photo: "Salt flats Bolivia" by psyberartist is licensed under CC BY 2.0

Is there enough Lithium for Electric Vehicles and where does Lithium come from?

Writen by: Jindui Hong & Watcharapong Suwandumrong

The fast growth of electric vehicles, powered by the lithium-ion batteries, has driven the high demand of lithium. Tesla alone has planned to deliver 1 million cars in 2021 which will require the supply of at least 50,000 tons Lithium Carbonate Equivalent (LCE) (https://www.cierra.com/news&events/innovation/19). The global Li demand is forecasted to be 1.7 million tons LCE by 2030, which will increase further to 5.0 million tons LCE by 2040.1 So a question has been raised: is there enough lithium for the electric vehicles?

According to United States Geological Survey, the global Li reserve is 113 million tons (LCE) while global lithium resource is 464 million tons (LCE), which is still increasing due to the continuous exploration.2 Therefore, there is plenty of lithium resources but there is going to be shortage of battery grade lithium supply to meet the demand because not every lithium source is equal. It has been noted that the forecast of lithium supply has been overstated, especially for the battery grade lithium.3 Lithium mining itself is a long period process, even the expansion of the capacity in an established project will take more than one year to complete, not to mention those greenfield projects that will typically take several years from the initial exploitation to go through several stages of feasibility studies, to engineering and construction, first production, and battery grade qualification. The impact of COVID-19 on the logistics and labour has made this worse which causes delays in either existing project capacity expansion or new project delivery timeline. According to Benchmark Mineral Intelligence, there could be shortage of lithium supply as early as 2024.

Image Source: Unsplash

In addition to the supply shortage, there are at least two trends in the lithium supply chain: 1) the localisation of lithium supply and 2) the sustainable lithium mining. The current global lithium is from either a) hard rock lithium mining in Australia with post-conversion in China, which alone accounts of at least 91% of hard rock lithium globally;4 or B) brine lithium recovery mainly from so-called “Lithium Triangle”, although small fraction of brine lithium is also produced in US and China.

Image Source: Tom Fisk via Pexel

There are strong incentives to build local lithium supply chain due to the strategic importance of Li in the revolution of mobility electrification. For example, lithium has been listed as strategically important metal by the UK parliament,5 national strategic resource in China,6 critical raw material in the EU7 and most recently essential mineral in the US.8 It is now common referred to “white gold” or “oil of 21st century”.9 The other trend is the ethnical and sustainable mining. For example, EU has set regulations that all batteries produced or imported within the EU will have to present CO2 footprint. Li from conventional hard rock (spodumene) mining could produce as high as 7 times CO2 compared with historically available numbers10 and the other impact to local environment and community has lead to some opposition to the new mining project in hard rock.11 The sustainability of current solar evaporation projects in the Lithium triangle also remain a concern.

To meet the ramping up lithium demand and at the same time build a more local and sustainable lithium supply chain, Direct lithium Extraction (DLE) of lithium from brines is the most likely solution. Li containing brines can be found all around the world, from salar brines (Chile, Argentina, Bolivia, US, China, etc.), to geothermal brines (US, UK, Germany, France, New Zealand, Philippines, Indonesia, etc.), to oilfield brines (Canada, US, etc.). While solar evaporation is only applicable to limited geographies, DLE can unlock the global lithium resources by pushing the mineralogical barrier.12 In comparing with hard rock mining and solar evaporation, DLE has the advantages of less energy intensive, less CO2 emission, lower footprint and more likely to ramp up easily thanks to the possible modular design.

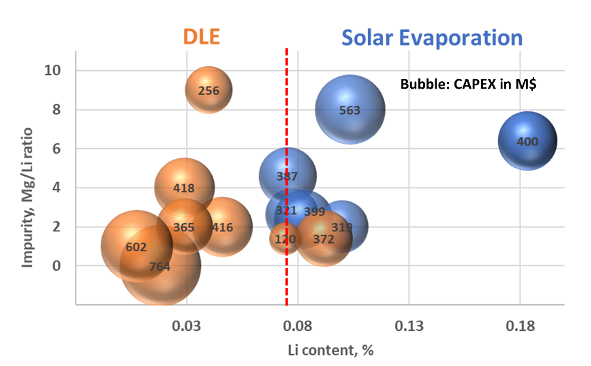

Figure 1. Brine Li recovery projects showing that solar evaporation projects can be found in > 750 ppm Li brines concentrated in Lithium Triangle while DLE projects are being developed in brine as low as 75 ppm.

From the announced projects, DLE’s contribution to global brine lithium production will increase from today’s 16% to at least 49% by 2025. To meet the lithium demand, at least 50 projects (based on 20,000 tons annual LCE production per project) need to be completed by 2030, majority of which are going to reply on the DLE technology.

References:

- https://piedmontlithium.com/wp-content/uploads/2146123-3.pdf

- https://pubs.usgs.gov/periodicals/mcs2021/mcs2021-lithium.pdf

- https://www.linkedin.com/pulse/why-most-analysts-overstating-lithium-supply-matt-fernley/?trackingId=QqR6OmsHTYSaL6JNUNn3cg%3D%3D

- https://www.statista.com/statistics/268789/countries-with-the-largest-production-output-of-lithium/

- https://publications.parliament.uk/pa/cm201012/cmselect/cmsctech/726/726.pdf

- http://extwprlegs1.fao.org/docs/pdf/chn189649.pdf (In Chinese)

- https://ec.europa.eu/growth/sectors/raw-materials/specific-interest/critical_en

- https://www.whitehouse.gov/briefing-room/statements-releases/2021/06/08/fact-sheet-biden-harris-administration-announces-supply-chain-disruptions-task-force-to-address-short-term-supply-chain-discontinuities/#

- https://dialogochino.net/en/extractive-industries/30612-lithium-puts-south-america-at-a-crossroads/

- https://www.jadecove.com/research/liohco2impact

- https://www.charlotteobserver.com/news/business/article252902968.html

- https://medium.com/batterybits/is-there-enough-lithium-to-make-all-the-batteries-c3a522c01498

Introduction to a new 2D material: layered double hydroxid...

The interesting move of brand owners to Paper Packaging

By employing this new class of inorganic adjuvants, more e...